Understanding the Reverse Charge Mechanism (RCM) under GST

The Goods and Services Tax (GST) has been a game-changer for the Indian economy, streamlining the tax structure and eliminating cascading taxes. However, within the GST framework, there is a unique provision known as the Reverse Charge Mechanism (RCM), which shifts the responsibility of paying tax from the supplier to the recipient of goods or services. This article delves deeper into the definition, application, key features, and impact of RCM on businesses, providing a comprehensive understanding of this important aspect of GST.

What is Reverse Charge Mechanism (RCM)?

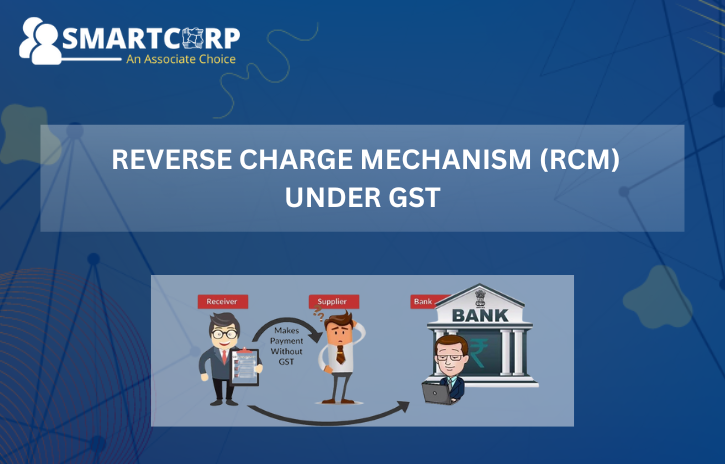

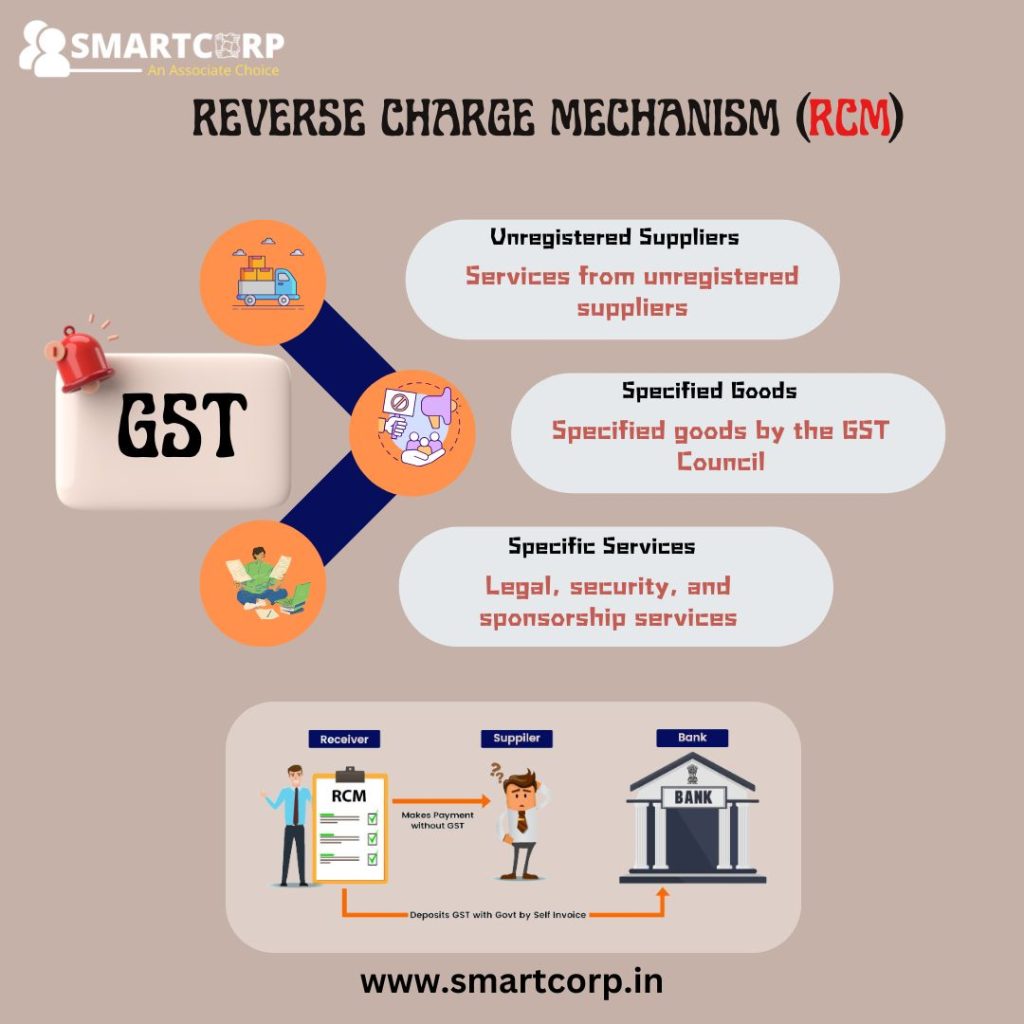

The Reverse Charge Mechanism (RCM) is a GST registration provision where the responsibility for paying tax is transferred from the supplier of goods or services to the recipient. In the typical forward charge mechanism, the supplier is responsible for collecting and depositing the GST with the government. However, under RCM, the buyer (recipient) becomes liable to pay the GST directly to the government. This is especially significant in cases where the supplier is unregistered under GST or where the nature of goods or services is prone to tax evasion.

The primary purpose of RCM is to ensure tax compliance in sectors that may otherwise escape the tax net. It encourages businesses to be more vigilant in tracking their purchases and tax payments and helps the government tap into the informal sector more effectively.

When Does RCM Apply?

RCM applies under specific circumstances as notified by the GST Council. Some of the most common scenarios include:

1. Services from Unregistered Suppliers

If a registered GST holder receives services from an unregistered supplier, the liability to pay GST shifts to the recipient. For instance, if a GST company in coimbatore hires a small contractor who is not registered under GST, the company will be responsible for paying GST on the services received.

2. Goods Specified by the GST Council

Certain goods, as notified by the GST Council, are subject to RCM. These include goods that are often prone to tax evasion due to their nature or the industries they belong to. Some examples include tobacco products, cashew nuts, silk yarn, and lottery tickets.

3. Services under Specific Categories

Certain services, especially those prone to tax evasion or provided by unregistered individuals, also fall under RCM. These include:

- Legal services provided by advocates to a business entity.

- Sponsorship services.

- Security services provided by an unregistered entity to a registered company.

- Goods transport services from an unregistered provider.

Key Features of RCM

Understanding the key features of the Reverse Charge Mechanism helps businesses navigate their tax obligations more effectively:

1. Tax Payment Responsibility

Under RCM, the recipient of goods or services has to self-invoice if the supplier is unregistered, meaning they generate a tax invoice on behalf of the supplier. The recipient must then pay the GST directly to the government, instead of relying on the supplier to collect and remit it. This requires businesses to track and report such transactions separately in their GST returns.

2. Compliance Requirements

RCM increases the compliance burden on the recipient of goods or services, as they must maintain accurate records of all purchases that fall under the RCM. Ensuring proper documentation and timely payment of GST under RCM is critical, as the burden of proof lies with the recipient to show compliance during audits or assessments.

3. Input Tax Credit (ITC)

While the recipient is responsible for paying the GST under RCM, they are also entitled to claim Input Tax Credit (ITC) on the tax paid, provided the goods or services are used for business purposes. This ITC can then be used to offset future GST liabilities, reducing the overall tax burden.

Impact of RCM on Businesses

RCM ensures tax payment at the point of consumption but brings certain implications for businesses, particularly impacting cash flow, increasing the administrative burden, and complicating compliance

1. Cash Flow Impact

One of the most significant challenges under RCM is the impact on cash flow. Businesses must pay the GST upfront when purchasing from an unregistered supplier, which can strain cash reserves, especially for small and medium-sized enterprises (SMEs).

2. Administrative and Compliance Burden

RCM increases the administrative burden on businesses. They must be vigilant about identifying which goods and services fall under RCM, maintain detailed records, and ensure timely payment of tax. This requires additional time, resources, and often specialized tax knowledge, adding to the cost of compliance.

3. Cost Implications

For businesses operating in sectors where RCM is applicable, the cost of compliance and tax payment can increase operational costs. This is particularly true if they regularly engage with unregistered suppliers or deal in goods prone to tax evasion. Businesses must factor these additional costs into their pricing and operational strategies.

Examples of Services Under RCM

- Legal Services: Legal services provided by an advocate or a law firm to a business entity are subject to RCM, meaning the business entity must pay the GST on behalf of the advocate.

- Security Services: If a company hires security personnel from an unregistered supplier, the company is liable to pay GST under RCM.

- Manpower Supply Services: When manpower supply services are provided by an unregistered supplier to a registered entity, the recipient must pay the GST under RCM.

- Goods Transport Services: If transportation services are provided by someone other than a body corporate, and the service provider is unregistered, the recipient of the service must pay GST under RCM.

Conclusion

The Reverse Charge Mechanism (RCM) plays a vital role in the GST framework, helping to reduce tax evasion and ensuring that tax is collected at the point of consumption.

While RCM shifts the tax liability from the supplier to the recipient, businesses must stay vigilant about their compliance obligations.

By understanding when RCM applies and keeping accurate records, businesses can effectively manage their tax liabilities while also claiming input tax credit for the GST paid under RCM.

RCM, though beneficial for overall tax collection, can increase cash flow pressures and administrative burdens, particularly for SMEs.

However, by maintaining sound tax practices and understanding the intricacies of RCM, businesses can navigate its challenges and ensure smooth compliance with GST laws.